15 August 2016, Yahoo 7 Finance:

Stephen Koukoulas

The banks are being blasted for not passing on in full the 25 basis point interest rate cut from the RBA earlier this month.

The government is so annoyed and outraged that it will be insisting the CEO’s of the Big Four banks will appear each year before a Parliamentary committee where they will have to explain their business operations, including how they determine their retail interest rate settings.

The Opposition Labor Party is ramping up its push for a Royal Commission into banking to determine whether or not banks are ripping off their customers.

Also read: Three ways Aussies can benefit from the banks’ war on deposits

Making matters uncomfortable for the banks is that fact that they are reporting their half-yearly profits at the moment. Those profits are big. So far it’s over $9.4 billion for the Commonwealth Bank and $5.2 billion for the ANZ.

The interesting issue with these spectacular headline results is the realisation that banks profits are not growing much and their cost of doing business, which clearly feeds into the interest rates they charge their customers, has not been falling to the same extent as the cuts in official interest rates.

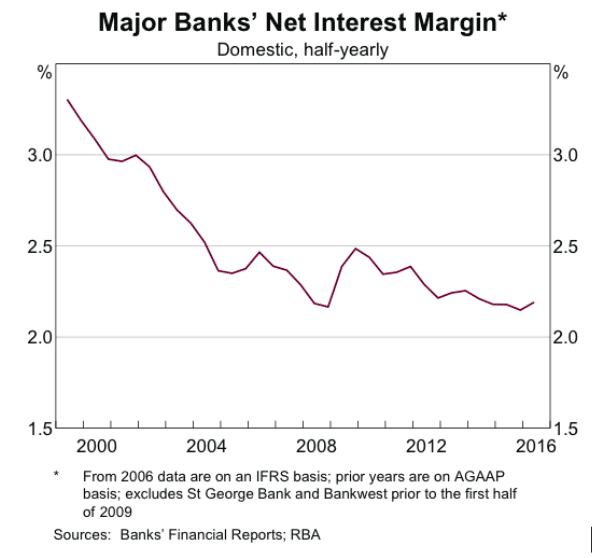

The chart from the recent RBA Chartpack shows how the banks’ net interest margin – the different between what banks pay to borrow money against the rate at which they lend to customers – it near historical lows. Margins are not widening – if anything, they are narrowing.

Let’s have a look why this is so.

In the current interest rate cutting cycle, the RBA has reduced the official cash rate from 4.75 per cent to 1.5 per cent, a fall of 325 basis points. Over the same timeframe, the standard variable mortgage interest rate has fallen by an average of about 260 basis points. In total, this means that about 65 basis points (or two and a half 25 basis point official interest rate cuts from the RBA) have seemingly pocketed by the banks.

Also read: Here’s how CBA managed to make a huge $9.45bn profit

I say “seemingly” because the issue is a little more complex that this.

Not that it gets much attention, but the banks have not passed on the official interest rate cuts to depositors. This is something that should be cheered by savers with interest earning deposits with the banks.

In the period where official interest rates have been cut by 325 basis points, the three month term deposit rates paid by the banks to savers, have only fallen by about 260 basis points, so the banks have given savers an extra 65 basis points.

And astute readers will be quick to see that the change in deposit rates is the same as the reduction on mortgage rates, which fits with the scenario of the interest margin being little changed in the current cycle of record low interest rates.

Also read: Before you switch from a Big Four bank, read this

Which goes to show that the banks are not ripping off customers any more now than they were in the past. The profit margins on the cost of doing business is relatively low, but has been little changed in recent years and while mortgage holders might be feeling somewhat annoyed at the fact that the banks have withheld about 65 basis points of interest rate cuts in the recent cycle, this is perfectly offset by the fact that depositors are receiving 65 basis points more than would have been the case if the banks had passed the rate cuts on in full to them.

Stephen Koukoulas is a Yahoo7 Finance expert with more than 25 years experience as an economist in government, as Global Head of economic and market research, as Chief Economist for two major banks, and as economic advisor to the Prime Minister of Australia.