By Osmond Chiu, Research Fellow

The recent interest rate hike to address inflation drifting above the Reserve Bank of Australia’s (RBA) target band has reignited debate about the Albanese Government’s economic management. Critics argue excessive government spending and the RBA’s initially slow response are to blame for rising prices and slower economic growth, despite the International Monetary Fund noting Australia is successfully managing a “soft” landing. New Liberal Opposition Leader Angus Taylor has blamed increased government spending for inflation, stating there is ‘no ambiguity’ that the Coalition’s solution would be to cut spending growth and the public service by at least 36,000.

But what if the RBA had lifted interest rates far more aggressively and what if the Albanese Government had implemented deep spending cuts as some commentators and the Coalition advocate?

New Zealand offers a revealing counterfactual.

Conservative politicians in Australia have often pointed to New Zealand’s current economic direction as a model. New Liberal Deputy Leader Jane Hume has praised the economic agenda of New Zealand’s right-wing government while Shadow Treasurer Tim Wilson has floated removing the RBA’s dual mandate so it focuses solely on inflation, mirroring New Zealand’s central bank (Wilson has already had second thoughts).

Yet New Zealand’s experience has been anything but exemplary. Since being elected in 2023, New Zealand’s most right-wing government since the 1990s has introduced sweeping austerity measures to fund tax cuts and limited spending to achieve a budget surplus. The NZ Treasury has warned that meeting the government’s 2028 surplus target without raising more revenue would require an unprecedented level of real and per-capita spending cuts, implying a fiscal savagery worse than that unleashed by Nationals Finance Minister Ruth Richardson in her ‘Mother of All Budgets’ of 1991 that destroyed New Zealand’s welfare state.

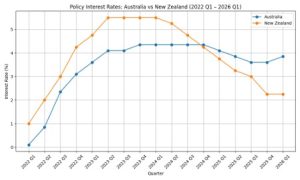

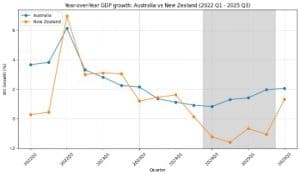

The Reserve Bank of New Zealand (RBNZ) also took a far more aggressive approach to monetary policy. It lifted rates rapidly to a peak of 5.5% in June 2023 and held them there for a full year. Rates have since been repeatedly slashed to 2.25%, primarily because New Zealand entered a double-dip recession in March 2024 (shown in the shaded chart) and the RBNZ sought to stimulate the economy. Australia has so far avoided recession altogether.

Despite these harsher policy settings, inflation in New Zealand has not meaningfully diverged from Australia’s inflation rate. Since 2022, both countries have experienced similar inflation trajectories, underscoring today’s sticky inflation is driven not mainly by domestic fiscal policy but by the tyranny of distance, geopolitical tensions, supply constraints, and sellers’ inflation. Even with deep spending cuts and after steep interest rate hikes, New Zealand’s inflation rate is now rising above its own inflation target band, a concept it arbitrarily pioneered and that many countries adopted. Crushing domestic demand has simply not delivered the promised results and will leave a generation economically scarred.

Where the two countries do diverge is in unemployment. Since the election of New Zealand’s conservative government in October 2023, unemployment there has climbed to 5.4%, the highest in a decade, even after consecutive interest rate cuts. In contrast, Australia’s unemployment rate has been fairly stable. In fairness to the RBNZ, it does not have a dual mandate to moderate both inflation and unemployment – unlike the RBA.

The social and political fallout is now impossible to ignore. New Zealanders endured the country’s worst downturn since the 1990s, with rising child poverty and widening inequality, the government showing little inclination to change course. Unsurprisingly, the first-term right-wing coalition government of conservatives, libertarians and right‑wing populists is now polling neck‑and‑neck with the centre‑left opposition.

Australia certainly needs economic reforms to tackle inflation, broaden the tax base, and ensure real wage growth. New Zealand’s experience, however, shows the “tough medicine” advocated by the Coalition and its fellow travellers of interest rate hikes and big cuts to public spending to suppress domestic demand is less a cure and more a poison pill. It risks even slower economic growth, much higher unemployment and the consequential greater strains on social cohesion, with little evidence it will tackle what is driving sticky inflation.